Demand and supply are fundamental concepts in economics that describe the relationship between the quantity of a good or service that consumers are willing to buy and the quantity that producers are willing to sell.

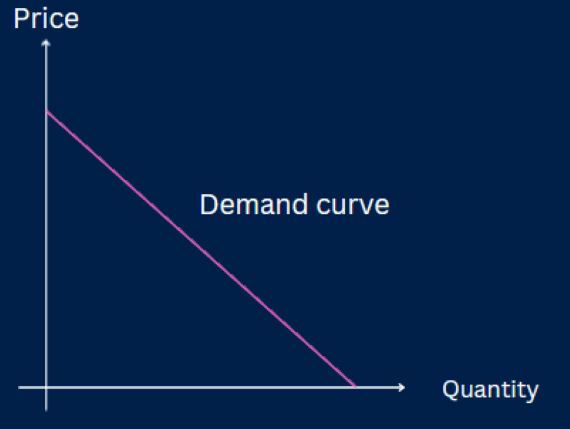

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various prices during a given period. There is an inverse relationship between price and quantity demanded, all else being equal. As the price of a good or service decreases, the quantity demanded increases, and vice versa.

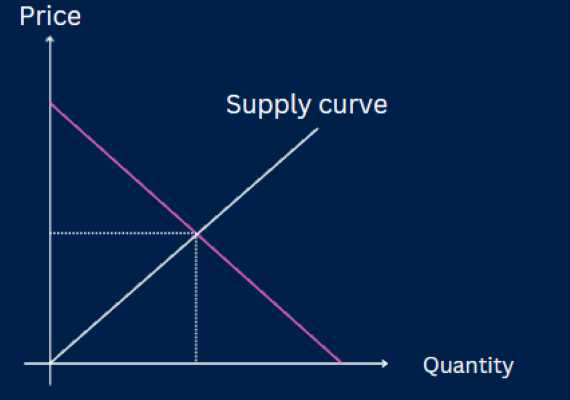

Supply refers to how much of a good or service producers are willing and able to sell at various prices. The supply curve is usually upward-sloping, indicating that as the price of a good increases, the quantity supplied increases, and vice versa.

Inflation is the rate at which the general level of prices for goods and services rises, leading to a decrease in the purchasing power of money. It reflects how much more expensive the relevant set of goods and services has become over a certain period, typically measured annually.

Higher wages can increase production costs if not matched by productivity gains

Prices of essential inputs like oil, metals, or agricultural products can rise.

Natural disasters, geopolitical events, or pandemics can disrupt production and supply chains, increasing costs

Depreciation of the local currency can make imported goods and services more expensive

Unemployment is a condition in which individuals who are capable of working, are actively seeking work, but are unable to find any work. It is a key indicator of the health of an economy and is typically measured by the unemployment rate, which is the percentage of the labor force that is unemployed and actively looking for employment.

Automation and new technologies can replace human labor, leading to job displacement in certain sectors

The movement of jobs to countries with cheaper labor can lead to job losses in higher-cost regions

Rapid population growth can lead to more individuals entering the labor market than there are jobs available

Physical or mental health problems can limit individuals' ability to work.

A monopoly is a market structure with a single seller or producer that assumes a dominant position in an industry or a sector. Monopolies are discouraged in free-market economies because they stifle competition, limit consumer substitutes, and thus, limit consumer choice.

Without competition, monopolies can set prices and keep pricing consistent and reliable for consumers

Monopolies enjoy economies of scale and often are able to produce mass quantities at lower costs per unit

Standing alone as a monopoly allows a company to securely invest in innovation without fear of competition

A company that dominates a sector or industry can use its advantage to create artificial scarcities, fix prices, and provide low-quality products

Due to limited or unavailable substitutes in the market, consumers have no option but to trust that a monopoly operates ethically

A monopsony is a market condition in which there is only one buyer, the monopsonist. Like a monopoly, a monopsony also has imperfect market conditions, being a unique form of market situation with distinctive features. Monopsonists are common in areas where they supply most of the region's jobs.

In a monopsony, there is only one buyer, which gives them significant market power and control over the price and quantity of goods or services purchased

Due to there being a single buyer that holds a majority of power, monopsonies mean sellers are relatively weak and have reduced bargaining power

Since the buyer has significant control over the market, there is less incentive for suppliers to invest in innovation or quality improvements

Market inefficiencies arise when the single consumer buys less of the good or service than would be produced in a more competitive market